Deflation

May 23rd, 2013 — 2:22am

Commentary on the spot FX markets

Submitted by Alasdair Macleod, via GoldMoney.com,

Introduction

In this article I will argue that the recent slide in the gold price has generated substantial demand for bullion that will likely bring forward a financial and systemic disaster for both central and bullion banks that has been brewing for a long time. To understand why, we must examine their role and motivations in precious metals markets and assess current ownership of physical gold, while putting investor emotion into its proper context.In the West (by which in this article I broadly mean North America and Europe) the financial community treats gold as an investment. However, of the global pool of gold, which GoldMoney estimates to be about 160,000 tonnes, the amount actually held by western investors in portfolios is a very small fraction of this amount. Furthermore investor behaviour, which in itself accounts for just part of the West’s bullion demand, is sharply at odds with the hoarders’ objectives, which is behind underlying tensions in bullion markets. To compound the problem, analysts, whose focus incorporates portfolio investment theories and assumptions, have very little understanding of the economic case for precious metals, being schooled in modern neo-classical economic theories.

These economic theories, coupled with modern investment analysis when applied to bullion pricing, have failed to understand the growing human desire for protection from monetary instability. The result has for a considerable time been the suppression of bullion prices in capital markets below their natural level of balance set by supply and demand. Furthermore, the value put on precious metals by hoarders in the West has been less than the value to hoarders in other countries, particularly the growing numbers of savers in Asia.

These tensions, if they persist, are bound to contribute to the eventual destruction of paper currencies.

The ownership of gold

The amount of gold bullion that backs investor-driven markets is not statistically recorded, but we can illustrate its significance relative to total stocks by referring back to the time of the oil crisis of the mid-1970s. In 1974 the global stock of gold was estimated to be half that of today, at about 80,000 tonnes. Monetary gold was about 37,000 tonnes, leaving 43,000 tonnes in the form of non-monetary bullion, coins and jewellery. Let us arbitrarily assume, on the basis of global wealth distribution, that two thirds of this was held by the minority population in the West, amounting to about 30,000 tonnes.

This figure probably grew somewhat before the early 1980s, spurred by the bull market and growing fear of inflation, which saw investors buy mainly coins and mining shares. Demand for gold bars was driven by the rapid accumulation of dollars in the oil-exporting nations, as well as some hoarding by wealthy investors from all over the world through Switzerland and London.

The sharp rise in global interest rates in the Volcker era, the subsequent decline of the inflation threat and the resulting bear market for gold inevitably led to a reduction of bullion holdings by wealthy investors in the West. Swiss and other private banks, employing a new generation of fund managers and investment advisors trained in modern portfolio theories, started selling their customers’ bullion positions in the 1980s, leaving very little by 2000. In the latter stages of the bear market, jewellery sales in the West became a replacement source of bullion supply, but this was insufficient to compensate for massive portfolio liquidation.

So by the year 2000, Western ownership of non-monetary gold suffered the severe attrition of a twenty-year bear market and the reduction of inflation expectations. Portfolios, which routinely had 10-15% exposure to gold 40 years ago even today have virtually no exposure at all. Given that jewellery consumption in Europe and North America was only 400-750 tonnes per annum over the period, by the year 2000 overall gold ownership in the West must have declined significantly from the 1974 guesstimate of 30,000 tonnes. While the total gold stock in 2000 stood at 128,000 tonnes, the virtual elimination of portfolio holdings will have left Western holders with little more than perhaps an accumulation of jewellery, coins and not much else: bar ownership would have been at a very low ebb.

Since 2000, demand from countries such as India and more recently China is known to have increased sharply, supporting the thesis that gold has continued to accumulate at an accelerating pace in non-Western hands.

Western bullion markets have therefore been on the edge of a physical stock crisis for some time. Much of the West’s physical gold ownership since 2000 has been satisfied by recycling scrap originating in the West, suggesting that total gold ownership in the West today barely rose before the banking crisis despite a tripling of prices. Meanwhile the disparity between demand for gold in the West compared with the rest of the world has continued, while the West’s investment management community has been actively discouraging investment.

The result has been that nearly all new mine production and Western central bank supply has been absorbed by non-Western hoarders and their central banks. While post-banking crisis there has presumably been a pick-up in Western hoarding, as evidenced by ETF and coin sales and some institutional involvement, it is dwarfed by demand from other countries. So it is reasonable to conclude that of the total stock of non-monetary gold, very little of it is left in Western hands. And so long as the pressure for migration out of the West’s ownership continues, there will come a point where there is so little gold left that futures and forwards markets cease to operate effectively. That point might have actually arrived, signalled by attempts to smash the price this month.

This admittedly broad-brush assessment has important implications for the price stability essential to bullion banks operating in paper markets as well as for central banks attempting to maintain confidence in their paper currencies.

Precious metals in capital marketsIn the West itself, the attitudes of the investment community are fundamentally different from even those of the majority of Western hoarders, who are looking for protection from systemic and currency risks as opposed to investment returns. Western investors are generally oblivious to the implications, the most fundamental of which is that falling prices actually stimulate physical demand. Before the recent dramatic slide in prices the investment community undervalued precious metals compared with Western hoarders, let alone those in Asia, encouraging physical bullion to migrate from financial markets both to firmer hands in the West as well as the bulk of it to non-West ownership. There is now irrefutable evidence that these flows have accelerated significantly on lower prices in recent weeks, as rational price theory would lead one to expect.

Pricing bullion is therefore not as simple as the investment community generally believes. It is being put about, mostly on grounds of technical analysis, that the bull markets in gold and silver have ended, and precious metals have entered a new downtrend. The evidence cited is that medium and longer-term moving averages have been violated and are now falling; furthermore important support levels have been breached.

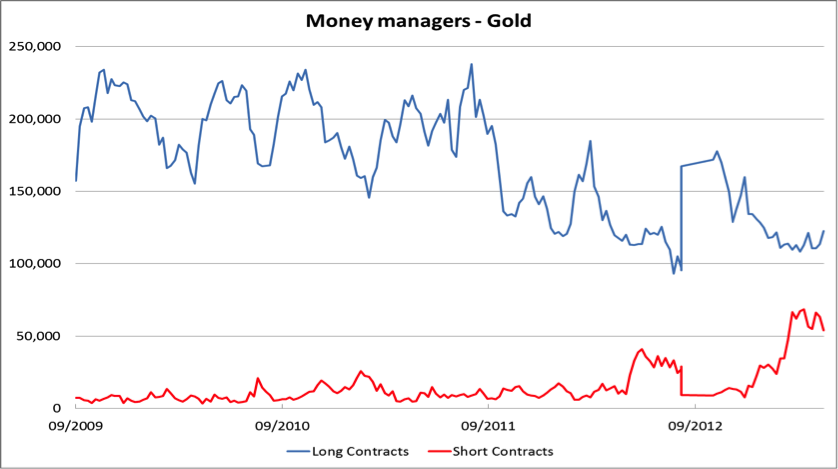

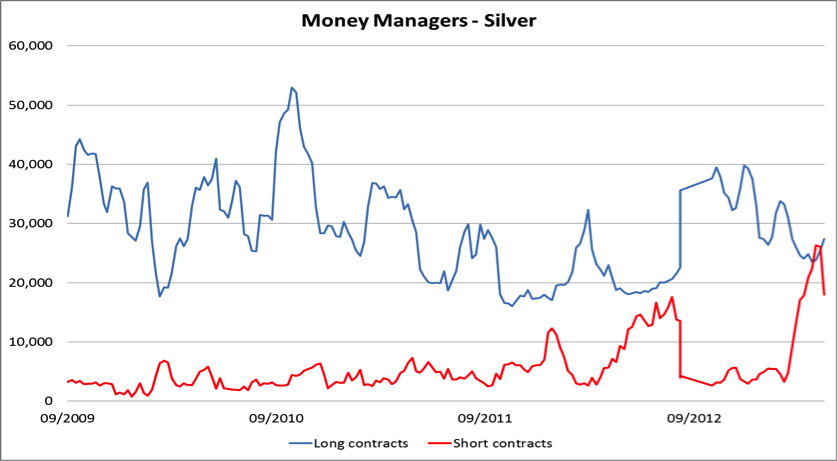

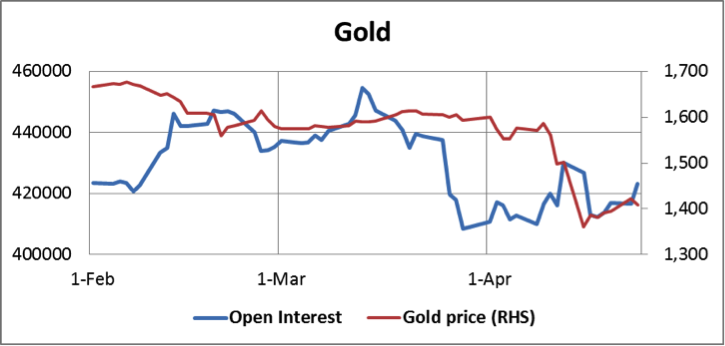

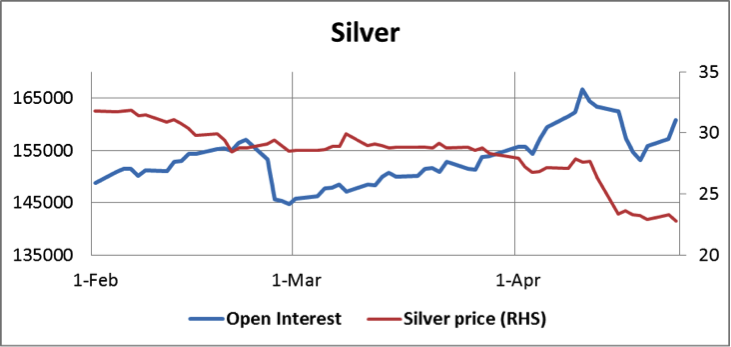

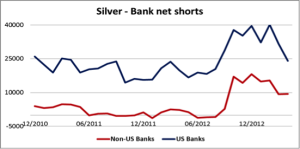

These developments, which arise out of the futures and forward markets, have rattled Western investors who thought they were in for an easy ride. However, a close examination of futures trading shows the bearish case even on investment grounds is flawed, as the following two charts of official statistics provided by weekly Commitment of Traders data clearly show.

The Money Managers category is the clearest reflection in the official data of investor portfolio positions, representing sizeable mutual and hedge funds. In both cases, the number of long contracts is at historically low levels, and shorts, arguably the better reflection of money-manager sentiment, remain close to high extremes. On this basis, investor sentiment is clearly very bearish already, with the investment management community already committed to falling prices. Put very simplistically there are now more buyers than sellers.

Money Managers are in stark opposition to the Commercials, who seek to transfer entrepreneurial risk to Money Managers and other investor and speculator categories. The official statistics break Commercials down into two categories: Producer/Merchant/Processor/User, and Swap Dealers. Both categories include the activities of bullion banks, which in practice supply liquidity to the market. Because investors and speculators tend to run bull positions, bullion banks acting as market-makers will in aggregate always be short. A successful bullion bank trader will seek to make trading profits large enough to compensate for any losses on his net short position that arise from rising prices.

A bullion bank trader must avoid carrying large short positions if in his judgement prices are likely to rise. He will be more relaxed about maintaining a bear position in falling markets. Crucially, he must keep these opinions private, and the release of market statistics are designed to accommodate these dealers’ need for secrecy.

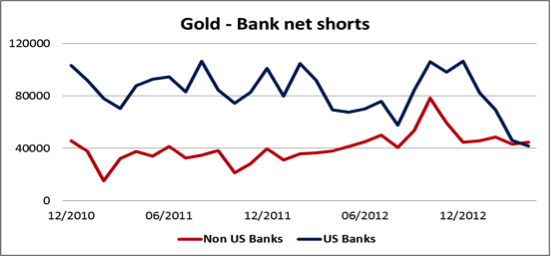

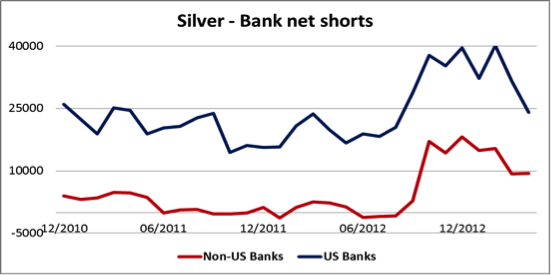

Bullion banks’ position details are disclosed at the beginning of every month in the Bank Participation Reports, again official statistics. They are broken down into two categories, based on the individual bank’s self-description on the CFTC’s Form 40, into US and Non-US Banks. Their positions are shown in the next two charts (note the time scale is monthly).

In both gold and silver, the bullion banks have managed to reduce their exposure from extreme net short over the last four months. The reduction of their market exposure suggests that they have been deliberately transferring this risk to other parties, and is consistent with an anticipation that bullion prices will rise. It is the other side of the high level of bearishness reflected in the Money Manager category shown in the first two charts. The bullion banks control the market; the Money Managers are merely tools of their trade.

There has been little reduction in open interest in gold and it has remained strong in silver, because risk has been transferred rather than extinguished. Daily official statistics on open interest are provided by the exchange and summarised in the next two charts (note that data is daily).

From these charts it can be seen that recent declines in the gold price are failing to reduce open interest further, and in silver open interest remains stubbornly high. Therefore, attempts by bullion banks to reduce their net short exposure by marking prices down are showing signs of failure.

We can therefore conclude that investor sentiment is at bearish extremes and the bullion banks have reduced their net short exposure to levels where it risks rising again. Therefore the downside for precious metals prices appears to be severely limited, contrary to sentiments expressed by technical analysts and in the media.

This market position is against a background of a growing shortage of physical bullion, which is our next topic.

Physical markets

Casual observers of precious metal prices are generally unaware that the headline writers focus on activity in the futures markets and generally ignore developments in physical bullion. This is consistent with the fact that market data is available in the former, while dealing in the latter is secretive. However, as with icebergs, it is not what you see above the water that matters so much as that which is out of sight below.

It is not often understood in investment circles that gold and silver are commodities for which the laws of supply and demand are not overridden by investor psychology. Therefore, if the price falls, demand increases. Indeed, the increase in demand has far outweighed selling by nervous investors; even before the price-drop, demand for both silver and gold significantly exceeded supply. Evidence ranges from readily available statistics on record demand for newly-minted gold and silver coins and the net accumulation of gold by non-Western central banks, to trade-based information such as imports and exports of non-monetary gold as well as reports from trade associations reporting demand in diverse countries such as India, China, the UK, US, Japan and even Australia.

All this evidence points in the same direction: that physical demand is increasing on every price drop. There is therefore a growing pricing conflict between futures and forward markets, which do not generally involve settlement but the rolling-over of speculative positions, and of the underlying physical metal. Furthermore, analysts make the mistake of looking at gold purely in terms of mining and scrap supply, when nearly all gold ever mined is theoretically available to the market, in the right conditions and at the right price. The other side of this larger coin is that if the price of gold is suppressed by activity in paper markets to below what it would otherwise be, the stimulus for physical demand, being based on a 160,000 tonne market, is likely to be considerably greater on a given price drop than analysts who are myopic beyond 2,750 tonnes of annual mine production might expect. The numbers that are available confirm this to have been the case, particularly over the last few weeks, with reports from all over the world of an unprecedented surge in demand.

This is at the root of a developing crisis of which few commentators are as yet aware. Demand for physical has accelerated the transfer of bullion from capital markets to hoarders everywhere and from the West’s capital markets to other countries, which has been the trend since the oil crisis in the mid-Seventies. This is what’s behind an acute shortage of physical gold in capital markets, explaining perhaps why bullion banks feel the need to reduce their short positions.

While we can detail their exposure in futures markets, meaningful statistics are not available in over-the-counter forward markets, particularly for London, which dominates this form of trading. Forwards are considerably more flexible than futures as a trading medium, generating trading profits, commissions, fees and collateralised banking business. The ability to run unallocated client accounts, whereby a client’s gold is taken onto a bank’s balance sheet, is in stable market conditions an extremely profitable activity, made more profitable by high operational gearing. The result is that paper forward positions are many multiples of the physical bullion available. The extent of this relationship between physical bullion and paper is not recorded, but judging by the daily turnover in London there is an enormous synthetic short physical position. For this reason a sharply rising price would be catastrophic and any drain on bullion supplies rapidly escalates the risk.

Overseeing this market is the Bank of England co-operating with other Western central banks and the Bank for International Settlements, whose combined interest obviously favours price stability. They have been quick to supply the market if needed, confirmed by freely-admitted leasing operations in the past, and by secretive supply into the market, which has been detected by independent supply and demand analysis over the last 15 years. Furthermore, as currency-issuing banks, central banks are unlikely to take kindly to market signals that suggest gold is a better store of value than their own paper money.

We can only speculate about day-to-day interventions by Western central banks in gold markets. In this regard it seems that the slide in prices on the 12th and 15th April was triggered by a very large seller of paper gold; if this market story and the amount mentioned are correct, it can only be central bank intervention, acting to deliberately drive prices lower. Given the market position, with Money Managers in the futures markets already short and highly vulnerable to a bear squeeze, the story seems credible. The objective would be to persuade holders of physical ETFs and allocated gold accounts to sell and supply the market, on the assumption that they would behave as investors convinced the bull market is over.

Conclusions

For the last 40 years gold bullion ownership has been migrating from West to elsewhere, mostly the Middle East and Asia, where it is more valued. The buyers are not investors, but hoarders less complacent about the future for paper currencies than the West’s banking and investment community. There was a shortage of physical metal in the major centres before the recent price fall, which has only become more acute, fully absorbing ETF and other liquidation, which is small in comparison to the demand created by lower prices. If the fall was engineered with the collusion of central banks it has backfired spectacularly.

The time when central banks will be unable to continue to manage bullion markets by intervention has probably been brought closer. They will face having to rescue the bullion banks from the crisis of rising gold and silver prices by other means, if only to maintain confidence in paper currencies. Any gold held by struggling eurozone nations, theoretically available to supply markets as a stop-gap, will not last long and may have been already sold.

This will likely develop into another financial crisis at the worst possible moment, when central banks are already being forced to flood markets with paper currency to keep interest rates down, banks solvent, and to finance governments’ day-to-day spending. Its importance is that it threatens more than any other of the various crises to destabilise confidence in government-backed currencies, bringing an early end to all attempts to manage the others systemic problems.

History might judge April 2013 as the month when through precipitate action in bullion markets Western central banks and the banking community finally began to lose control over all financial markets.

Basically what he’s saying is that, just as the credit markets consist of so much fractional fiat on top of very little of value, so the unallocated forward market for physical gold now consists of many multiples of actual physical reserves having been sold forward.

The credit markets will cease to function as assets supporting extended credit get wiped out leading to waves of bank insolvency rippling through the banking system. When this happens, J.P. Morgan’s comment that “Money is gold and nothing more” will become bleedin’ obvious and the bullion banks will then be hit by unmeetable demands for delivery of the forward sold bullion.

Should be fun. Or not.

Originally posted on ZeroHedge here

Jamie Dimon Has Issues

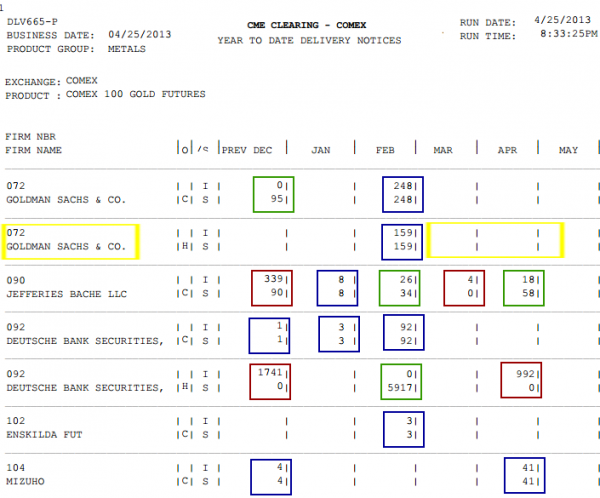

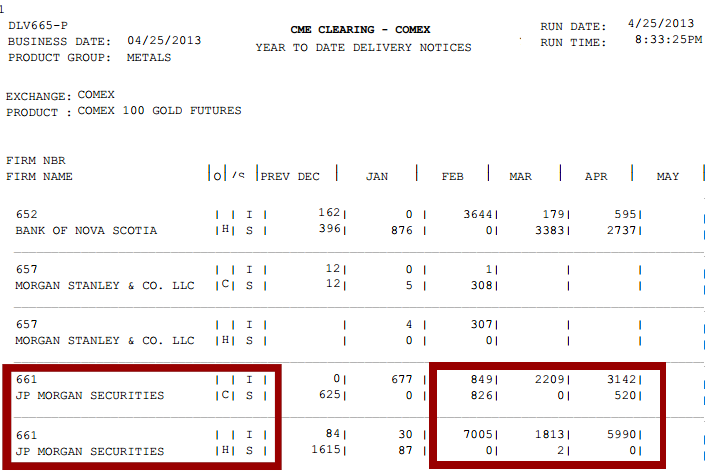

When just one firm accounts for 99.3% of the physical gold sales at the COMEX in the last three months it’s not what most of us on this side of the rainbow would consider “broad-based” selling. Of course discovering this kind of relevant information requires an internet connection, 2nd grade math and reading skills, and the desire to do a teeny-weeny bit of reporting. Sadly they’ve wandered so far down the rabbit hole that the concept of “physical demand” (i.e. people actually wanting to take possession of the stuff) is puzzling to them because the vast majority of the world’s so-called “gold-trading” takes place in the realm of make believe (which is their natural habitat). It’s all fun and games until somebody loses their metal and “somebody” has lost one hell of a lot of metal in the last 90 days.

This is the CME Group’s COMEX metals issues and stops year-to-date report, which can be found here everyday for free. It chronicles the physical delivery notices of various metals, including gold. Let’s have a look:

“I” is for “Idiot”

That’s how I remember it, anyway. “I” actually stands for “issues,” meaning the firm parted with its metal (@ 100 troy ounces a shot), and “S” stands for “stops,” meaning the firm took delivery of gold. “C” is for customer accounts, “H” is house accounts. The first thing you should notice is that most transaction net out to zero in a given month (blue boxes), meaning the firm’s gold holdings didn’t change. What they delivered one day they got back the next, or vice versa. The green boxes show firms who received more than they delivered and the red boxes indicate firms who coughed up gold for Bernanke bucks (aka idiots). Note that Deutsche Bank’s massive take in February more than offsets its deliveries in December and April.Notice one more thing before we move on: Despite Goldman’s much ballyhooed “Gold Sucks!” call a few weeks ago, the squid has not parted with any yellow metal whatsoever in 2013. Hmmm.

Now for the main event:

J P Morgan has fumbled ownership of 1,966,000 Troy ounces of gold since February 1. That’s 74% more gold than the US mint delivered through the US mint’s American Eagle program in all of 2012. I mention this because there’s little doubt in my mind that the US government is one of JPM’s gold “customers.” So (if I am correct) the same US government who just let the Morgue dump its gold on the COMEX floor will once again be suspending gold sales to peasants.

Maybe Jamie Dimon figures he’ll buy back all that gold on the cheap when the rest of the world realizes how smart he is. Or maybe he’s once again displaying that his firm doesn’t have the slightest idea what “hedging” is and is teetering on the brink of collapse. That would explain the April 11th meeting between President Obama and the Pig 5 bank CEOs, wouldn’t it? And you just have to get a little misty that Lloyd Blankfein was nice enough to provide some hot-air cover for his competitor, don’t you?

One thing’s very clear: When it comes to selling physical gold, J P Morgan is acting alone. The 130 contracts NOT delivered by JPM in the last three months (of which 110 were fromABN AMRO) are but a footnote. If Jamie’s right, he’ll look like a genius in a few months, if not he should be able to recycle his quote regarding the infamous “London Whale” losses: “Just because we’re stupid, doesn’t mean everybody else was.” Time will tell.

100 years ago John Pierpont Morgan famously testified to Congress, “Money is gold, and nothing else.” (Note: That is the exact quote, the full testimony can be found here). One has to wonder what the big guy would think of his legacy’s disregard for sound money, $70 Trillion derivatives book, and “House of Cards” “Fortress” balance sheet.

One more very, very important thing.

Anybody who says there’s been gold selling in the GLD is a freaking moron (Bob Pistrami, I’m looking in your direction). The GLD works much like a coat check. Unless you think checking your coat constitutes a real transaction of some kind you shouldn’t think of changes in the GLD’s gold holdings as sales. They’re not. When you check your gold into the GLD you get shares (like a claim check). Where it gets wierd is you can sell these claim checks to nimrods who seem to think they’ve bought your coat, but aren’t actually allowed to wear it.What nobody seems to appreciate is that every share of GLD is allowed to be sold TWICE (long and short, and it’s really important to understand that). If you’re foolish enough to doubt me (and foolish enough to short gold), go short GLD shares and see if anyone knocks on your door demanding gold. Saying the GLD is 100% backed by gold is a bold face lie because they’re can be twice as many shares in play as gold backing them, which means GLD shares may be only 50% backed by gold before any rules are broken.

When GLD (or any ETF for that matter) shares sold exceed the existing shares PLUS all the shortable (double-sold) shares, legitimate shares can not be found for settlement and that must be reported to the SEC’s “Fails to Deliver” list, which is published twice a month with about a four-week delay (here).

April 15, 2013 was this biggest volume day ever for GLD (93.7mm) and I’ll guarantee you right now that record fails to deliver will be reported on or around that date, which should have required more gold to be deposited with the GLD (but that didn’t happen). So instead of the half-assed explanation Pistrami offered (here) of how he thinks the GLD works, he should have raised the question of whether or not there were enough legitimate shares of GLD to facilitate trading (I say no way in hell).

Gold continues to be pulled from the GLD (which really means people want their coats back) and still no one’s concerned about the number doubled-owned shares. Worse yet, the responsibility for sorting this unholy mess out falls to SEC chief Mary Jo White who is celebrating her 16th day in office.

I can’t wait to see what happens next….

Notes for Nerds: This piece is not intended to describe the inner workings of the COMEX or GLD in detail, so don’t bust my balls with minutiae, unless it is relevant to the discussion of JPM’s massive gold sales or the double-ownership of ETF shares. Double-owned ETF shares are huge problem with ETFs in general, but the misrepresentation (by omission) of this fact by ETFs supposedly backed by tangible assets like gold and silver seems more egregious to me.

In addition to the YTD CME Group metals report, you can track the hilarity on a day-by-day basis here.

The February 1 to April 25 delivered gold contracts info referenced included only transactions between firms. For that reason Morgan Stanley’s 307 contracts transferred from house account to customer account was excluded from the calculations.

Total Net gold deliveries Feb 1 to April 25:

Vision Financial – 1 contract

R J O’Brien – 2

ADM Investor Services INC – 2

Marex – 5

Citigroup Global Markets – 10

ABN AMRO – 110

JP Morgan – 19,660

So the US government is trying to re-acquire Gold, and they want to do it highly visibly on Comex so the selling can drive the price down. Do they have a plan for when the physical runs out ?

Interesting comments on GLD as well.

In summary, own physical and keep it away from the banking and exchange system as eventually the govt will just come and steal it. They’re dangerous and stupid.

Originally posted here

Comex to go bankrupt as it eventually dawns that there is not enough inventory to supply demand at current prices, leading to longs electing to take delivery, in turn leading to massive squeeze ?

One of the more curious revelations of the New Normal is the fundamental dichotomy when investing between paper “investors”, or those who chase returns based on intangible, fiat-based and central bank-backed promises, such as capital appreciation or cash flow streams, and those who would rather convert their paper money into hard assets, even if said assets can not be, in the immortal words of Warren Buffett, fondled, or otherwise generate a cash-based return. Such as gold.

Today provides perhaps the perfect example of how the former increasingly trade on nothing but momentum and speculative mania (such as the previously reported record inflow of foreign capital into the Japanese stock market well after the bulk of the easy upside has already been made and at this point there is mostly downside) and where buying begets only more buying, while rampant selling only leads to liquidations, while those who invest in hard assets (and thus have little to no leverage) have become the true value investors, purchasing more as the price of the underlying asset drops. Yes, a novel concept to most High Frequency Trading vacuum tubes, and the momentum-chasing, equity trading “expert” du jour, but nothing new to Indians, Australians, Chinese or the Japanese.

And apparently to at least some Americans.

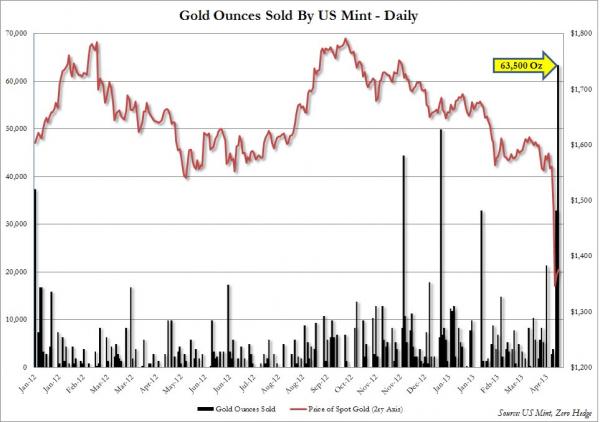

According to today’s data from the US Mint, a record 63,500 ounces, or a whopping 2 tons, of gold were reported sold on April 17th alone, bringing the total sales for the month to a whopping 147,000 ounces or more than the previous two months combined with just half of the month gone.

Punchline number one, as the chart below shows, is that the more the price of gold fell, the more aggressive the purchases of physical gold through the Mint became, rising to 96,500 oz in the last two days alone. Buying more of something you want when the price drops: what a stunning concept – explain that to the algos who nearly crashed the German stock market overnight.

Punchline number two, of course, is that the US mint charges a hefty premium for purchases: much more so than traditional vendors like Apmex or Gainesville Coins, and is usually the last resort for when nobody else has any physical at a lower premium to spot (or any metal in inventory).

So how long until the US mint “runs out” of American Eagles and Buffaloes in inventory, along with the depletion of all other precious metal vendors? And what happens if the price of paper gold hits zero (or goes negative) courtesy of bank and financial institution liquidation selling of paper derivative contracts nebulously referencing some yellow metal somewhere, even as suddenly there is no physical to be delivered to anyone, anywhere?

Inquiring minds really want to know.

Ex-Soros Advisor Sells “Almost All” Japan Holdings, Shorts Bonds; Sees Market Crash, Default And Hyperinflation

From zerohedge here

Previously, we have pointed out why Japan’s attempt at reincarnating its economy, geared solely at generating a stock market-based “wealth effect”, and far less focused on boosting the country’s trade surplus or current account, is doomed to failure, namely due the drastically lower equity participation by the general population and financial institutions in the country’s stock market. Sure, foreign investors will come and go renting each rally for a period of time, but unless the local population participates in the “reflation attempt” (which has already sent the price of luxury goods, energy and food through the rood), or in other words change the behavioral patterns of two generations of Japanese in under two years, the inflationary shock will simply leads to a loss of faith in the government and ultimately Abe’s second untimely demise. Not surprisingly, 4 months after Japan set off on the most ludicrous economic experiment in history, and one week after the BOJ announced its plans to double its balance sheet, Abe’s approval rating has already begun sliding with a poll by Asahi just reporting that popular support of Abe’s cabinet is already down to 60%, down from 71% a month ago.

The reflationary reality has finally started to get official recognition with the very Goldman Sachs (who like in Europe and the US is behind this epic experiment in hidden taxation of consumers) asking how popular inflation would be in Japan, and answers:

How popular will inflation be in Japan? Assuming the BoJ is successful and inflation rates rise, one interesting dynamic will be the political support for ‘super-easy’ monetary policy. The majority of financial household assets sit in deposits, which until now have earned a positive real rate. While long-term inflation expectations move higher, the Yen and equities re-price rapidly but the negative impact on deposit returns from negative real rates will only be felt once inflation has actually started to materialise. This is clearly not an immediate concern as the government’s approval ratings remain high ahead of the Upper House elections this Summer. Still, PM Abe’s policy aim of beating deflation may become less popular at some stage because the implied distributional choices of higher inflation may become clearer for voters. For example, higher inflation would re-distribute real income from (older) savers to (younger) wage earners. But again it is worth thinking about the exact sequencing. By the time inflation in Japan becomes settled in positive territory the Fed may well be on the verge of hiking rates. In essence, any concerns about inflation in Japan and debate about a BoJ policy response will likely arrive at a stage when Fed tightening and JPY carry trades have already become the dominant theme.

In short, yes, Japanese inflation will destabilize the economy, and almost certainly lead to yet another political upheaval, but by then Japan will have served its purpose and injected some $1 trillion into the US stock market, thus supposedly allowing the US economy to become self sustaining. Or not. As to the consequences that the demographically-challenged Japanese population has to face as it suddenly finds itself holding worthless pieces of paper… who cares.

Which means that Abenomics will ultimately fail to fix Japan, but at least there is some hope it will last long enough to send the S&P to even more ridiculous highs – which, when one cuts out all the noise, it really what the whole experiment is all about.

For Japan, there is still some hope that the country will stop this ludicrous experiment merely serving to feed US risk assets before it is too late. Luckly, we are not the only ones seeing the writing on the wall. A month ago, it was “Mr. Yen”, former finmin Eisuke Sakakibara, himself, saying “Abenomics” is going to fail.

“In terms of two percent inflation, it [‘Abenomics’] will fail. Deflation is structural. Even at the time, when Japan was in the upward [growth] swing between 2002 and 2007, prices went down. It will be extremely difficult to get out of deflation,” said Sakakibara, also known as “Mr. Yen” for his efforts to influence the currency’s exchange rate through verbal and official intervention in the forex markets in the late 1990s.

According to Sakakibara structural deflation in the world’s third largest economy is largely a result of the integration between the Japanese and Chinese economies and hence near impossible to move away from.

“Cheap Chinese goods come into Japan and push down the prices. And a lot of Japanese companies go to China to manufacture goods — so it’s not going to change,” said Sakakibara, who is currently a professor at Aoyama-Gakuin University in Tokyo.

According to Sakakibara, dollar-yen between 90 and 95 would be most favorable for the economy.

“I remember in 1998, 1999 — it [dollar-yen] did go to 150 — I was at that time in the government, I was terrified,” he said.

Moments ago, it was none other than Takeshi Fujimaki, Soros’ former advisor on all matters Japanese, who tripled down on the warnings, and told Bloomberg that the Bank of Japan’s “huge bet” by boosting quantitative easing won’t turn the economy around and is instead sending the nation toward default.

“By expanding the monetary base to 270 trillion yen, the BOJ is making a huge bet which I think it will ultimately lose,” Fujimaki said in an interview in Tokyo on April 11. “Kuroda’s QE announcement is declaring double suicide with the government. The BOJ will have to share the country’s fate and default together.”

Why? Same reason we have been pointing out every day for the past week, the same reason the Japanese bond market is now essentially broken with daily trading halts becoming an expected feature:

“The volatility in the JGB market as well as the fact that there is large selling represent fear among investors,” Fujimaki said. “They are early signs of a larger selloff and we should continue to monitor the moves in the long-term bonds.”

Fujimaki said he recently bought put options for Japanese government bonds of various maturities, without elaborating. He continues to hold real estate in Japan and options granting the right to sell the yen against the greenback expiring in less than five years. He also holds assets in U.S. dollars and currencies of other developed nations.

“Japan’s finance is sinking into the ocean,” Fujimaki said. “There’s no escape from a market crash in the future when you have such enormous debt.”

And the punchline:

“By expanding the monetary base to 270 trillion yen, the BOJ is making a huge bet which I think it will ultimately lose,” Fujimaki said in an interview in Tokyo on April 11. “Kuroda’s QE announcement is declaring double suicide with the government. The BOJ will have to share the country’s fate and default together.”

“Shirakawa did more than enough and he had good reasons to not do any more,” said Fujimaki. “There will be tremendous side effects from monetary stimulus. QE doesn’t work and has no exit.”

“Things may look rosy for now as stocks rise, but should we see hyper-inflation, JGBs will see a huge selloff, leading to a stock market crash,” said Fujimaki, adding that he sold “almost all” of his Japanese stock holdings some time ago.

Wow.

And people thought Kyle Bass was bearish.

Great stuff in Gold yesterday as the market finally broke the multiple lows which have been in place since mid 2011, and continued its correction. This should flush out some ‘weak longs” and set up a test of the 1396 – 1404 area.

Click to expand.

There’s still so much excess debt that deflation is still the dominant force.

a recent update from gains, pains and capital.

China Just Threatened a Currency War If the Fed Doesn’t Stop Printing

The tension between Central Banks that we noted yesterday continues to worsen. This time it was China and the EU, not just Germany, that fired warning shots at the US Fed.

A senior Chinese official said on Friday that the United States should cut back on printing money to stimulate its economy if the world is to have confidence in the dollar.

Asked whether he was worried about the dollar, the chairman of China’s sovereign wealth fund, the China Investment Corporation, Jin Liqun, told the World Economic Forum in Davos: “I am a little bit worried.”

“There will be no winners in currency wars. But it is important for a central bank that the money goes to the right place,” Li said.

Speaking at the same session, French Finance Minister Pierre Moscovici voiced concern that the euro was becoming overvalued as a result of quantitative easing and other stimulus actions taken by other nations’ central banks.

“Certainly, the level of the euro is high and creates some problem,” he said, attributing the single currency’s recent gains partly to the return of confidence created by the European Central Bank and euro zone governments in starting to overcome Europe’s debt crisis.

Source: Reuters.

So first Germany begins pulling its Gold reserves from the US, and now China and the EU are saying publicly that the Fed’s policies are damaging confidence in the US Dollar.

This does not bode well for the financial system. The primary role of Central Banks is to maintain confidence in the system. If the Central Banks begin to turn on one another it is only a matter of time before the system breaks down.

Remember, every time the Fed debases the US Dollar it forces the Euro and other currencies higher, hurting those countries’ exports. The Fed has recently announced it will be printing $85 billion every month until employment reaches 6.5% (obviously the Fed is ignoring the mountains of data that indicate QE doesn’t create jobs).

How long will the other Central Banks tolerate this before they initiate a currency war? Both Germany and China have fired warning shots at the Fed. And we all know that just beneath the veneer of goodwill, tensions are building between the primary players of the global financial system.

Comment » | Asia, Geo Politics, QE, US denouement, USD

originally posted here and here

Authored by Detlev Schlichter; originally posted at DetlevSchlichter.com,

We are now five years into the Great Fiat Money Endgame and our freedom is increasingly under attack from the state, liberty’s eternal enemy. It is true that by any realistic measure most states today are heading for bankruptcy. But it would be wrong to assume that ‘austerity’ policies must now lead to a diminishing of government influence and a shrinking of state power. The opposite is true: the state asserts itself more forcefully in the economy, and the political class feels licensed by the crisis to abandon whatever restraint it may have adhered to in the past. Ever more prices in financial markets are manipulated by the central banks, either directly or indirectly; and through legislation, regulation, and taxation the state takes more control of the employment of scarce means. An anti-wealth rhetoric is seeping back into political discourse everywhere and is setting the stage for more confiscation of wealth and income in the future.

War is the health of the state, and so is financial crisis, ironically even a crisis in government finances. As the democratic masses sense that their living standards are threatened, they authorize their governments to do “whatever it takes” to arrest the collapse, prop up asset prices, and to enforce some form of stability. The state is a gigantic hammer, and at times of uncertainty the public wants nothing more than seeing everything nailed to the floor. Saving the status quo and spreading the pain are the dominant political postulates today, and they will shape policy for years to come.

Unlimited fiat money is a political toolA free society requires hard and apolitical money. But the reality today is that money is merely a political tool. Central banks around the world are getting ever bolder in using it to rig markets and manipulate asset prices. The results are evident: equities are trading not far from historic highs, the bonds of reckless and clueless governments are trading at record low interest rates, and corporate debt is priced for perfection. While in the real economy the risks remain palpable and the financial sector on life support from the central banks, my friends in money management tell me that the biggest risk they have faced of late was the risk of not being bullish enough and missing the rallies. Welcome to Planet QE.

I wish my friends luck but I am concerned about the consequences. With free and unlimited fiat money at the core of the financial industry, mis-allocations of capital will not diminish but increase. The damage done to the economy will be spectacular in the final assessment. There is no natural end to QE. Once it has propped up markets it has to be continued ad infinitum to keep ‘prices’ where the authorities want them. None of this is a one-off or temporary. It is a new form of finance socialism. It will not end through the political process but via complete currency collapse.

Not the buying and selling by the public on free and uninhibited markets, but monetary authorities – central bank bureaucrats – now determine where asset prices should be, which banks survive, how fast they grow and who they lend to, and what the shape of the yield curve should be. We are witnessing the destruction of financial markets and indeed of capitalism itself.

While in the monetary sphere the role of the state is increasing rapidly it is certainly not diminishing in the sphere of fiscal policy. Under the misleading banner of ‘austerity’ states are not rolling back government but simply changing the sources of state funding. Seeing what has happened in Ireland and Portugal, and what is now happening in Spain and in particular Greece, many governments want to reduce their dependence on the bond market. They realize that once the bond market loses confidence in the solvency of any state the game is up and insolvency quickly becomes a reality. But the states that attempt to reduce deficits do not usually reduce spending but raise revenues through higher taxes.

Sources of state fundingWhen states fund high degrees of spending by borrowing they tap into the pool of society’s savings, crowd out private competitors, and thus deprive the private sector of resources. In the private sector, savings would have to be employed as productive capital to be able repay the savers who provided these resources in the first place at some point in the future. By contrast, governments mainly consume the resources they obtain through borrowing in the present period. They do not invest them in productive activities that generate new income streams for society. Via deficit-spending, governments channel savings mainly back into consumption. Government bonds are not backed by productive capital but simply by the state’s future expropriation of wealth-holders and income-earners. Government deficits and government debt are always highly destructive for a society. They are truly anti-social. Those who invest in government debt are not funding future-oriented investment but present-day state consumption. They expect to get repaid from future taxes on productive enterprise without ever having invested in productive enterprise themselves. They do not support capitalist production but simply acquire shares in the state’s privilege of taxation.

Reducing deficits is thus to be encouraged at all times, and the Keynesian nonsense that deficit-spending enhances society’s productiveness is to be rejected entirely. However, most states are not aiming to reduce deficits by cutting back on spending, and those that do, do so only marginally. They mainly replace borrowing with taxes. This means the state no longer takes the detour via the bond market but confiscates directly and instantly what it needs to sustain its outsized spending. In any case, the states’ heavy control over a large chunk of society’s scarce means is not reduced. It is evident that this strategy too obstructs the efficient and productive use of resources. It is a disincentive for investment and the build-up of a productive capital stock. It is a killer of growth and prosperity.

47 percent, then 52 percent, then 90 percent…Why do states not cut spending? – I would suggest three answers: first, it is not in the interest of politicians and bureaucrats to reduce spending as spending is the prime source of their power and prestige. Second, there is still a pathetic belief in the Keynesian myth that government spending ‘reboots’ the economy. But the third is maybe the most important one: in all advanced welfare democracies large sections of the public have come to rely on the state, and in our mass democracies it now means political suicide to try and roll back the state.

Mitt Romney’s comment that 47% of Americans would not appreciate his message of cutting taxes and vote for him because they do not pay taxes and instead rely on government handouts, may not have been politically astute and tactically clever but there was a lot of truth in it.

In Britain, more than 50 percent of households are now net receivers of state transfers, up 10 percent from a decade ago. In Scotland it is allegedly a staggering 90 percent of households. Large sections of British society have become wards of the state.

Against this backdrop state spending is more likely to grow than shrink. This will mean higher taxes, more central bank intervention (debt monetization, ‘quantitative easing’), more regulatory intervention to force institutional investors into the government bond market, and ultimately capital controls.

Eat the Rich!In order to legitimize the further confiscation of private income and private wealth to fund ongoing state expenditure, the need for a new political narrative arose. This narrative claims that the problem with government finances is not out-of-control spending but the lack of solidarity by the rich, wealthy and most productive, who do not contribute ‘their fair share’.

An Eat-the-Rich rhetoric is discernible everywhere, and it is getting louder. In Britain, Deputy Prime Minister Nick Clegg wants to introduce a special ‘mansion tax’ on high-end private property. This is being rejected by the Tories but, according to opinion polls, supported by a majority of Brits. (I wager a guess that it is popular in Scotland.) In Germany, Angela Merkel’s challenger for the chancellorship, Peer Steinbrueck, wants to raise capital gains taxes if elected. In Switzerland of all places, a conservative (!) politician recently proposed that extra taxes should be levied on wealthy pensioners so that they make their ‘fair’ contribution to the public weal.

France on an economic suicide missionThe above trends are all nicely epitomized by developments in France. In 2012, President Hollande has not reduced state spending at all but raised taxes. For 2013 he proposed an ‘austerity’ budget that would cut the deficit by €30 billion, of which €10 billion would come from spending cuts and €20 billion would be generated in extra income through higher taxes on corporations and on high income earners. The top tax rate will rise from 41% to 45%, and those that earn more than €1 million a year will be subject to a new 75% marginal tax rate. With all these market-crippling measures France will still run a budget deficit and will have to borrow more from the bond market to fund its outsized state spending programs, which still account for 56% of registered GDP.

If you ask me, the market is not bearish enough on France. This version of socialism will not work, just as no other version of socialism has ever worked. But when it fails, it will be blamed on ‘austerity’ and the euro, not on socialism.

As usual, the international commentariat does not ‘get it’. Political analysts are profoundly uninterested in the difference between reducing spending and increasing taxes, it is all just ‘austerity’ to them, and, to make it worse, allegedly enforced by the Germans. The Daily Telegraph’s Ambrose Evans-Pritchard labels ‘austerity’ ‘1930s policies imposed by Germany’, which is of dubious historical and economic accuracy but suitable, I guess, to make a political point.

Most commentators are all too happy to cite the alleged negative effect of ‘austerity’ on GDP, ignoring that in a heavily state-run economy like France’s, official GDP says as little about the public’s material wellbeing as does a rallying equity market in an economy fuelled by unlimited QE. If the government spent money on hiring people to sweep the streets with toothbrushes this, too, would boost GDP and could thus be labelled economic progress.

At this point it may be worth adding that despite all the talk of ‘austerity’ many governments are still spending and borrowing like never before, first and foremost, the United States, which is running the largest civil government mankind has ever seen. For 5 consecutive years annual deficits have been way in excess of $1,000 billion, which means the US government borrows an additional $4 billion on every day the markets are open. The US is running budget deficits to the tune of 8-10% per annum to allegedly boost growth by a meagre 2% at best.

Regulation and more regulationFiscal and monetary actions by states will increasingly be flanked by aggressive regulatory and legislative intervention in markets. Governments are controlling the big pools of savings via their regulatory powers over banks, insurance companies and pension funds. Existing regulations already force all these entities into heavy allocations of government bonds. This will continue going forward and intensify. The states must ensure that they continue to have access to cheap funding.

Not only do I expect regulation that ties institutional investors to the government bond market to continue, I think it will be made ever more difficult for the individual to ‘opt out’ of these schemes, i.e. to arrange his financial affairs outside the heavily state-regulated banking, insurance, and pension fund industry. The astutely spread myth that the financial crisis resulted from ‘unregulated markets’ rather than constant expansion of state fiat money and artificially cheap credit from state central banks, has opened the door for more aggressive regulatory interference in markets.

The War on OffshorePart and parcel of this trend is the War on Offshore, epitomized by new and tough double-taxation treaties between the UK and Switzerland and Germany and Switzerland. You are naïve if you think that attacks on Swiss banking and on other ‘offshore’ banking destinations are only aimed at tax-dodgers. An important side effect of these campaigns is this: it gets ever more cumbersome for citizens from these countries to conduct their private banking business in Switzerland and other countries, and ever more expensive and risky for Swiss and other banks to service these clients. For those of us who are tax-honest but prefer to have our assets diversified politically, and who are attracted to certain banking and legal traditions and a deeper commitment to private property rights in places such as Switzerland, banking away from our home country gets more difficult. This is intentional I believe.

The United States of America have taken this strategy to its logical extreme. The concept of global taxation for all Americans, regardless where they live, coupled with aggressive litigation and threat of reprisal against foreign financial institutions that may – deliberately or inadvertently – assist Americans in lowering their tax burden, have made it very expensive and even risky for many banks to deal with American citizens, or even with holders of US green cards or holders of US social security numbers. Americans will find it difficult to open bank accounts in certain countries. This is certainly the case for Switzerland but a friend of mine even struggled obtaining full banking services in Singapore. I know of private banks in the UK that have terminated banking relationships with US citizens, even when they were longstanding clients. All of this is going to get worse next year when FATCA becomes effective – the Foreign Account Tax Compliance Act, by which the entire global financial system will become the extended arm of the US Internal Revenue System. US citizens are subject to de facto capital controls. I believe this is only a precursor to real capital controls being implemented in the not too distant future.

When Johann Wolfgang von Goethe wrote that “none are more hopelessly enslaved than those who falsely believe they are free” he anticipated the modern USA.

And to round it all off, there is the War on Cash. In many European countries there are now legal limits for cash transactions, and Italy is considering restrictions for daily cash withdrawals. Again, the official explanation is to fight tax evasion but surely these restrictions will come in handy when the state-sponsored and highly geared banking sector in Europe wobbles again, and depositors try to pull out their money.

“I’ve seen the future, and it will be…”So here is the future as I see it: central banks are now committed to printing unlimited amounts of fiat money to artificially prop up various asset prices forever and maintain illusions of stability. Governments will use their legislative and regulatory power to make sure that your bank, your insurance company and your pension fund keep funding the state, and will make it difficult for you to disengage from these institutions. Taxes will rise on trend, and it will be more and more difficult to keep your savings in cash or move them abroad.

Now you may not consider yourself to be rich. You may not own or live in a house that Nick Clegg would consider a ‘mansion’. You may not want to ever bank in Switzerland or hold assets abroad. You may only have a small pension fund and not care much how many government bonds it holds. You may even be one those people who regularly stand in front of me in the line at Starbucks and pay for their semi-skinned, decaf latte with their credit or debit card, so you may not care about restrictions on using cash. But if you care about living in a free society you should be concerned. And I sure believe you should care about living in a functioning market economy.

This will end badly.

Comment » | Deflation, Fed Policy, General, Geo Politics, Gold, Macro Structure, QE

GBPDEM from May to November 1992

Comment » | EU, Geo Politics, Gold, Macro, Sterling, The Euro